{kind=link}

matejmo/iStock via Getty Images

Denver-based Palantir Technologies Inc. (NYSE:PLTR) released its Q2 earnings after markets closed on the 5th of August. While analysts had estimated earnings per share (EPS) of $0.08 on revenue of $653 million, the company’s actual EPS of $0.09 was earned on the back of revenues of $678 million. Immediately following the earnings, the stock surged during both extended trading on the 5th and early trading on the 6th.

As it stands, trends as of the first half (H1) of the year have several milestones seemingly on the verge of being made.

Trend Drilldown

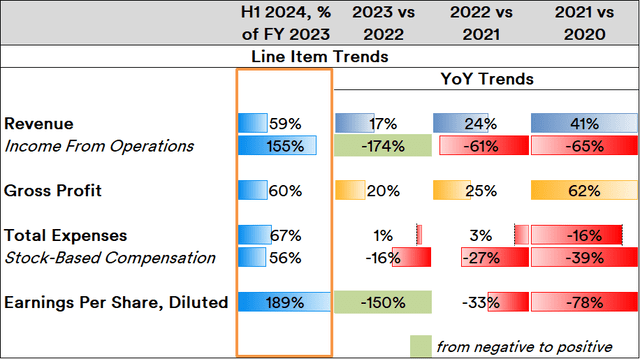

2023 was a transformative year for the company’s fortunes, with H1 2024 performance showing early trends of beating:

Source: Created by Sandeep G. Rao using data from Palantir’s Financial Statements

2023 was the year when operating income as well as EPS went from negative to positive, indicating that the company has turned a corner in building out its suite of services. In H1, revenue is trending to close out the year 18% higher, which was nearly the same growth rate seen in 2023, with gross profit also showing a similar trend regarding the previous year.

However, the growth in total expenses is spiking to be far higher than that seen in the previous year, with growth in stock-based compensation (“SBC”) seemingly poised to rise substantially for the first time since 2020. While the impact of SBC on EPS for the year remains to be seen, EPS trends outside of net effect considerations indicate that they will be quite strong. These are likely to be a net positive, unlike in all years before 2023.

Now, while Palantir Technologies Inc. CEO Alex Karp touted strong growth in the commercial user base in Q2, the picture is somewhat weakened when considering revenues across government and commercial segments:

Source: Created by Sandeep G. Rao using data from Palantir’s Financial Statements

As of H1, there is a slight shift in the revenue mix seen in 2023 in that 1% of total revenue has effectively shifted over to the commercial segment. However, the share of the government sector’s contribution has (in fact) increased in Q2 relative to Q1.

Breaking It All Down

As mentioned in an earlier article regarding the company’s Q4 earnings, it is moderately unfair to both the company and investors to describe Palantir as an “AI” company: while the company does own a number of AI-driven platforms, its business model is more akin to that of banks and management consulting firms wherein the highest expense (and the greatest driver of revenue) are the people on board to manage clients. If framed as an analogue to banks or management consulting firms, SBC becomes a vanishing concern. If framed as a “technology” firm, high SBC would evoke questions.

The company’s core competency does lie in harnessing technology to deliver insights for their clients, and its involvement with intelligence agencies spans well over a decade by now. This involvement, of course, makes a deep drilldown into determining its most successful practice or area difficult (if not impossible). In the course of the call, CEO Karp stated the company’s commitment to supporting U.S. interests in the region thus:

“The world is on the precipice of what could be a very severe set of violent interactions in the Middle East… It goes without saying that at Palantir, we know where we stand and we are very much supporting America and its allies in the Middle East, including Israel.”

With additional conflict being implied and its leadership position in delivering services to the government (and, by extension, the military and intelligence apparatus), the forward outlook on the company being able to monetize on this is quite rosy.

On the other hand, a number of analysts had flagged the fact that the current souring of institutional investor sentiment over continued corporate spends on AI-related projects where the actual benefits have consistently been low while overall outlay being promised is orders of magnitude greater than the computation engine of global digital infrastructure currently in operation. Some of these were highlighted in a recent article about TSMC, which highlights a likelihood of pullback on commercial spending, which impacts the forward outlook of this segment as proposed by Mr. Karp.

Over in the commercial segment, competition would be manifold and global. However, in the government segment, it’s likely that the company is included in a very short “preferred vendors” list. As it stands, the U.S. government is — by far — the biggest customer in the government segment: while total government revenues grew Year-on-Year (YoY) $69 million to $371 million in Q2 2024, revenue from the U.S. government alone grew by $53 million to $278 million (or about 75% of total government revenue).

In Conclusion

The prospect of conflict raising certain stocks isn’t limited to Palantir alone: Lockheed Martin (LMT) also rose in value in the course of overnight trading on the 5th because of a growing outlook that conflict, particularly in the Middle East, can be expected to grow. So, if the outlook is bearish for the company’s commercial segment, the government segment seems rather bullish.

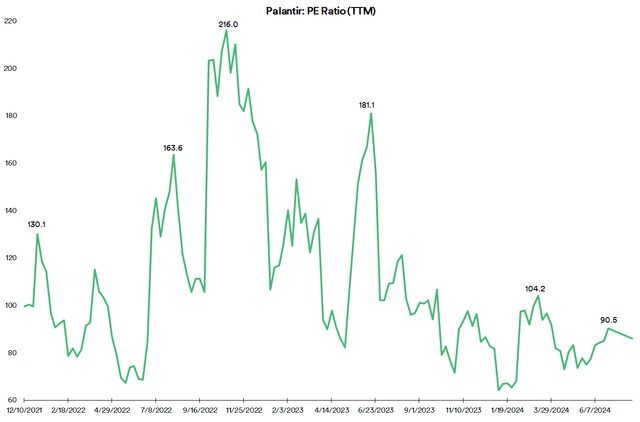

It also bears noting that the company’s stock valuation in Price to Earnings (PE) Ratio on in Trailing Twelve Month (TTM) terms has described a trajectory of massive swings over the past couple. This is steadily rationalizing, well, lower than that seen by the end of 2021.

Source: Created by Sandeep G. Rao using data from Zacks’

However, as of close of trading on the 5th, the company’s TTM PE Ratio is 54.2% higher than that of “AI champ” Nvidia (NVDA).

While neither revenue nor scale is comparable to that of Nvidia, it could be argued that Palantir’s reach and service offering to select niches within the U.S. government makes it a different proposition. Be that is it may, the company’s stock valuation will be tested, and price ratio rationalizations will likely continue.

All in all, a “hold” is in order for those who like the company’s mission statement and purpose. For those considering it for the “AI” exposure in the commercial realm, there will be competition; so it might be to diversify further.