{kind=link}

Arnold Media/DigitalVision via Getty Images

Introduction

I think there’s a lot of good value to be found in the Canadian REIT sector, so I’m keeping close tabs on several Canadian REITs in the retail, residential and industrial space. I used to own the convertible debentures of Plaza Retail REIT (TSX:PLZ.UN:CA) (OTC:PAZRF) but fortunately/unfortunately the REIT repaid the debentures on the maturity date. I’m obviously glad the REIT survived the COVID pandemic but I also didn’t mind getting a decent coupon from a well-run REIT. But as interest rates on the financial markets have been increasing, Plaza Retail also had and has to deal with an increasing cost of debt. This means I need to keep a close eye on Plaza’s quarterly performance to make sure the generous dividend isn’t at risk.

This article is meant as an update to previous articles, which you can find here.

The Q1 performance

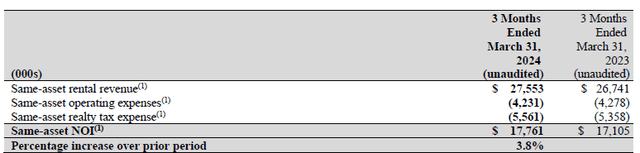

Looking at the Q1 performance, the assets are performing as expected. Plaza Retail was able to record a YoY net increase of the same-asset net operating income by approximately 3.8% to C$17.8M.

Plaza Investor Relations

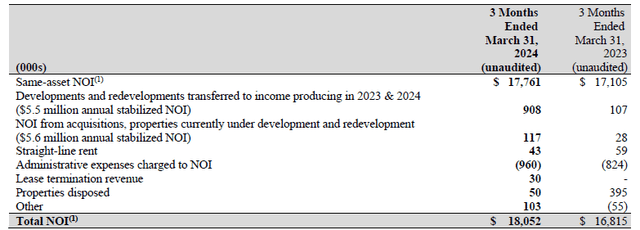

That being said, Plaza also invested in additional space while there are also some specific G&A items that are charged to the NOI performance. As you can see below, this added close to a million Canadian dollars to the NOI result. The total NOI was approximately C$18.05M.

Plaza Investor Relations

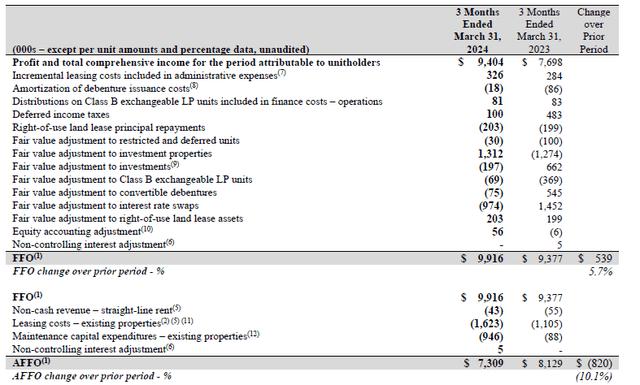

When looking at a REIT, the FFO and AFFO result are obviously more important than the net profit is. As you can see below, Plaza Retail was actually able to post a substantial increase in its FFO performance, which jumped by almost 6% to C$9.9M, coming from just C$9.4M in the first quarter of last year.

Plaza Investor Relations

This resulted in an FFO per share of approximately C$0.089/share which is pretty much in line with the result last year as the higher average share count reduces the impact on the per-share performance.

In Canada, the AFFO calculation also includes maintenance capex. As you can see in the image above, there was approximately C$0.95M in maintenance capex while there were about C$1.6M in lease-related expenses. This definitely weighed on the AFFO result which decreased by approximately 10% to C$7.3M which indicates an AFFO of C$0.066 per share. That’s disappointing, but keep in mind these expenses were extraordinarily high in the first quarter as the maintenance capex and leasing costs more than doubled compared to the first quarter of last year. I’m looking forward to seeing how these costs evolve over the next few quarters. I expect them to trend down, which will immediately result in an increasing AFFO, as the Q1 AFFO was not sufficient to cover the monthly dividend of C$0.0233/share.

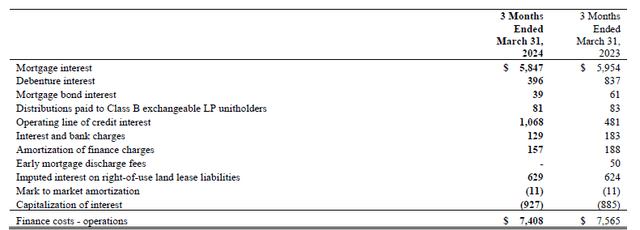

One of the main questions in the current investment climate is how the interest rates will impact the FFO and AFFO further down the road. As you can see below, the REIT paid about C$5.85M in mortgage interest and C$1.07M in interest on the credit facility. I will zoom in on these two elements as they represent the majority of the total interest expense.

Plaza Investor Relations

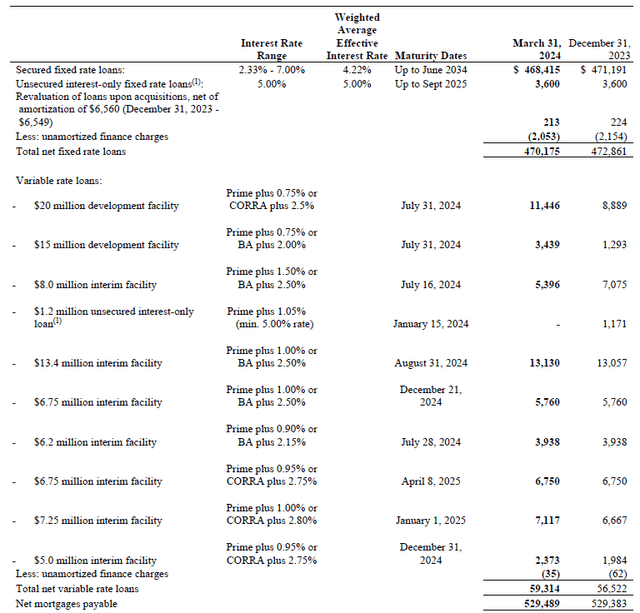

At the end of Q1, the REIT had just under C$530M in mortgages outstanding which means the average weighed cost of the mortgages was approximately 4.4%. As you can see below, the vast majority of the mortgages has a fixed interest rate, with 4.22% as average, but with interest rates ranging from 2.3% to 7%, with maturity dates spread out over the next decade. Plaza obtained a new 10-year mortgage during the first quarter of the year, and was able to lock in a 5.69% interest rate.

Plaza Investor Relations

The credit facility is a more expensive form of debt as the facility has an interest rate of prime + 0.75% or Bankers acceptance plus 2%. This credit line matures in the third quarter of this year and it will be interesting to see the terms to renew the line of credit. I expect Plaza to once again have a floating rate credit facility to take advantage of the potentially decreasing interest rates on the financial markets.

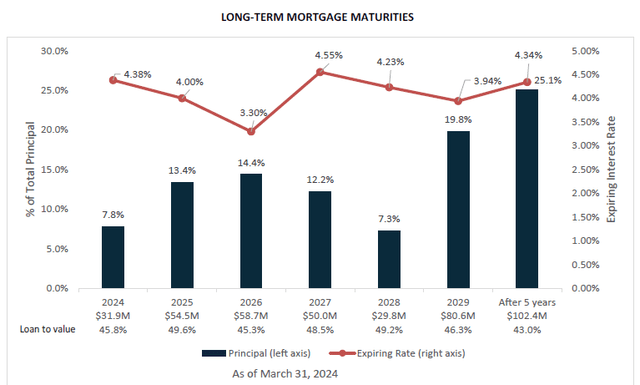

Between now and the end of 2026, the REIT only has to refinance approximately C$145M in mortgages. These have a weighted average interest rate of 3.8% so I think it’s fair to assume the average cost of debt will increase by 100-150 bp on these refinancings over the next three years (assuming the company is able to refinance its 2026 maturities at lower rates than in 2024 and 2025 given the anticipation to see lower interest rates on the financial markets). That would represent approximately C$2M per year in additional interest expenses by the end of 2026.

Plaza Investor Relations

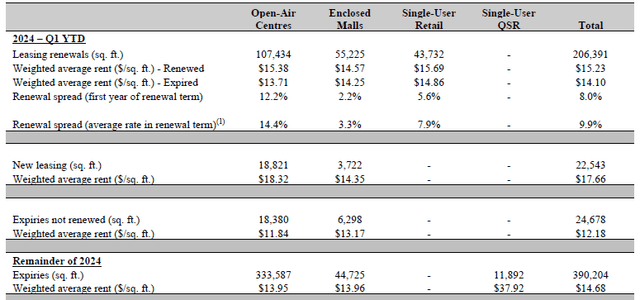

I expect the REIT to be able to compensate the higher interest expenses with higher rental income. The leasing spreads were pretty impressive in the first quarter of the year as Plaza reported an average renewal spread of 9.9%, fueled by the open air centers where the renewal spread exceeded 14%.

Plaza Investor Relations

As you can see in the image above, there are in excess of 330,000 square feet that are up for renewal in the remaining three quarters of the year. It will be interesting to see the renewal spreads on those renewals as some have contractual terms but others will be repriced at market. As you can see below, an additional 1.47 million square feet will be up for renewal in 2025 and 2026, and further rent hikes should allow Plaza to cover the aforementioned anticipated interest expense increases.

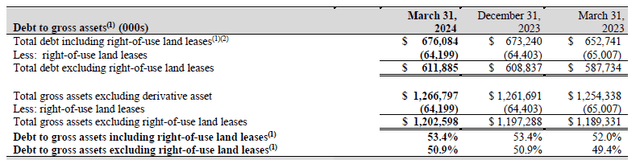

At the end of Q1, the REIT had approximately C$9M in cash, and C$676M in liabilities for approximately C$667M in net financial liabilities (including lease liabilities). Offset by about C$1.23B in assets and investments, the LTV ratio is approximately 54.5%. The REIT publishes a gross debt to assets ratio (which is not entirely the same as it keeps the cash as an asset instead of calculating a net debt position), resulting in a 53.4% debt ratio including leases and 50.9% excluding leases.

Plaza Investor Relations

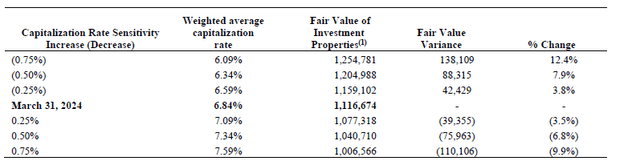

While that’s a relatively high LTV ratio, keep in mind the properties are valued at a very reasonable capitalization rate. As you can see below, the average cap rate was 6.84%. And even if you would increase the cap rate to 7.59%, the balance sheet would only lose about C$110M in value. That’s less than 10%, which means the LTV ratio would remain below 60%.

Plaza Investor Relations

On the other hand, if the interest rates and capitalization rates would moderate in the future and the REIT is able to use a lower cap rate of, for instance 6.50%, it would likely add about C$58M in value.

Investment thesis

As of the end of Q1 2024, the book value per share was approximately C$4.95 (including the impact of the C$4.2M in Class B Exchangeable LP Units on the share count). This means the stock is currently trading at a discount of approximately 25% to its book value. At the current share price the dividend yield is approximately 7.6% and although the distribution was not fully covered by the AFFO result in the first quarter of 2024, I think the full-year result will cover the distribution as the maintenance capex and leasing expenses in the first quarter of the current year were relatively high.

I currently have no position in Plaza Retail REIT as I have been favoring other Canadian REITs recently. Plaza is cheap from a NAV perspective and attractive from an income perspective. But based on its AFFO performance with an AFFO per share of C$0.291 in FY 2023 and my expectations to see an AFFO of C$0.30 this year, the earnings multiple isn’t very low. But as mentioned before, the renewal spreads are pretty strong and this could hopefully boost the earnings somewhat.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.