{kind=link}

Bank OZK

Introduction

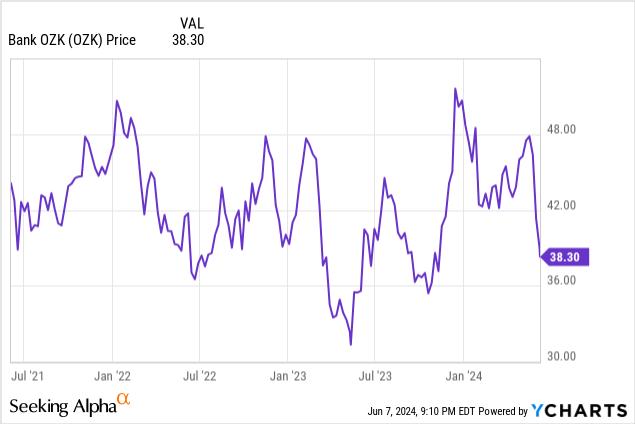

Bank OZK (NASDAQ:OZK) has had a tough time lately as the market continues to focus on the negative impact of commercial real estate on the bank’s loan book with fellow author Mark Dockray explaining how Citigroup (C) torpedoed OZK. While Bank OZK definitely has an overweight position in CRE as a portion of its total loan book, the average LTV ratio in that segment remains low. In fact, despite expanding the loan book in the first quarter of the year, the total amount of loans past due actually decreased. Meanwhile, the bank is guiding for record earnings this year, and that’s why I’m having a closer look at the preferred shares while also considering the common equity for an investment.

Yes, the balance sheet is exposed to CRE

Before discussing the bank’s balance sheet, I think it is important to have a closer look at its earnings profile first. After all, the higher the earnings, the higher the potential loan loss provisions the bank could set aside to cover potential losses.

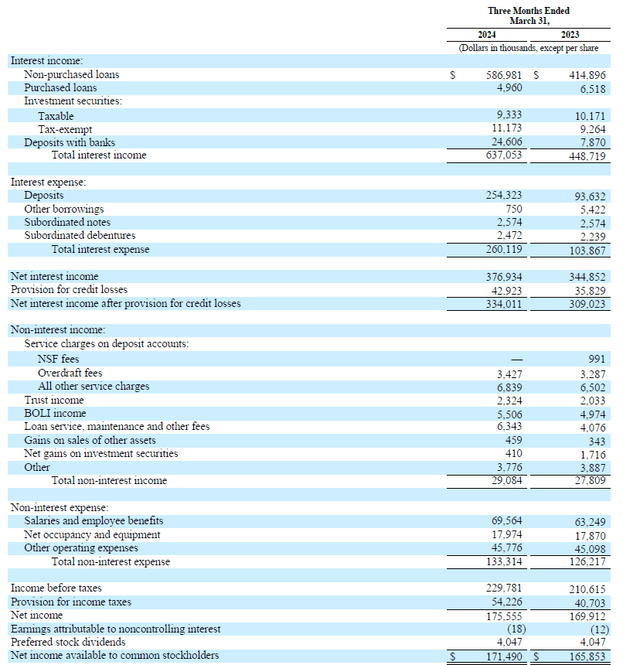

And that’s something Bank OZK is thriving at. As you can see below, the bank saw its interest income increase from less than $450M to in excess of $637M in the first quarter of the current financial year compared to Q1 2023. And although its total interest expenses increased as well, the net interest income increased from just under $345M to almost $377M, a $32M increase.

Bank OZK Investor Relations

Another excellent achievement is OZK’s ability to keep the other operating expenses under control. The non-interest income increased by just $1.2M, while the total amount of non-interest expenses jumped by just $7M. This allowed Bank OZK to report a pre-tax and pre loan loss provision income of almost $273M. Bank OZK recorded a $43M loan loss provision and a $54.2M tax bill, which resulted in a net profit of just over $175M.

From that amount, we still have to deduct the $4.05M in quarterly preferred dividend payments, which results in a Q1 net profit of $171.5M attributable to the shareholders of Bank OZK. This works out to $1.51 per share, representing a 6% increase compared to the EPS of $1.42 in the first quarter of 2023. It goes without saying the preferred dividends are very well covered as the bank needed less than 3% of its Q1 net profit to cover the preferred dividends.

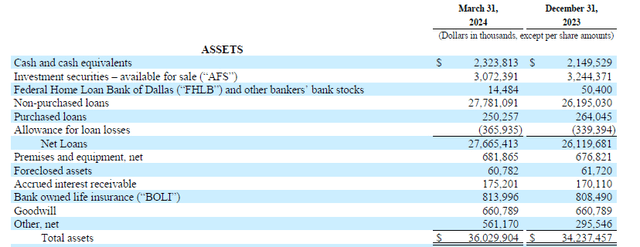

So, one of the most commonly heard arguments against an investment in Bank OZK is its exposure to commercial real estate. There’s no denying or sugarcoating; that is absolutely the case. Let’s have a look at the asset side of the balance sheet. As you can see below, the bank’s balance sheet has grown to just over $36B. The liquidity levels are okay, with close to $5.4B in cash and securities available for sale.

Bank OZK Investor Relations

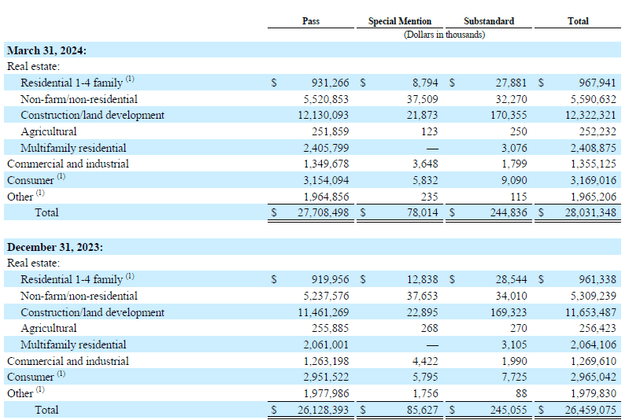

I am obviously more interested in the $27.7B loan book. As shown below, the vast majority of the loan book consists of commercial real estate. Of the $28B in loans (before taking provisions into account), Less than $325M are classified as a special mention or a substandard loan.

Bank OZK Investor Relations

While the bank has a very high exposure level to commercial real estate, there are two important elements here that work in OZK’s advantage.

First of all, the average LTV ratios are pretty low. The bank’s Real Estate Specialties Group is a leader in the CRE construction and development finance. The RESG division represents a total of $18B of the entire loan book and with an average loan to cost ratio of 52% and an average LTV ratio of around 43%, OZK’s CRE lending division is definitely keeping an eye on loan quality. As the bank explains, the loans in that category are typically the ‘last dollars to fund a project’ and the first dollars to be repaid. Meanwhile, some of the loans include mezzanine debt and preferred equity, which are both junior to the senior secured loans provided by the bank.

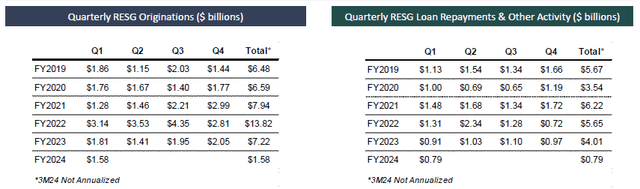

The image below shows the total impact of the repayments. As you can see, the bank issued almost $1.6B in new loans but also received $0.79B in repayments. This indeed means the CRE loan book is still growing but at a moderate pace and the newest loans will obviously be issued using more conservative valuation parameters.

Bank OZK Investor Relations

In other words, the almost $9B in CRE loans that were originated since the beginning of 2022 will likely have a lower risk level than the ‘older’ loans, and the $4.8B in cumulative loan repayments since the start of last year were likely tied to loans where the value of the underlying building already deteriorated.

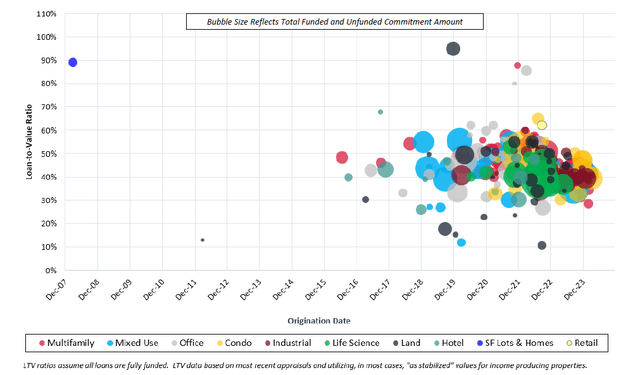

The image below also provides some clarity on the underwriting process. As you can see, most loans issued in the past three years had an LTV ratio in the 40-60% range. And the biggest problem child, office-related CRE, also has relatively low LTV ratios (excluding that one office loan issued in FY 2022 with an LTV ratio of close to 90%).

Bank OZK Investor Relations

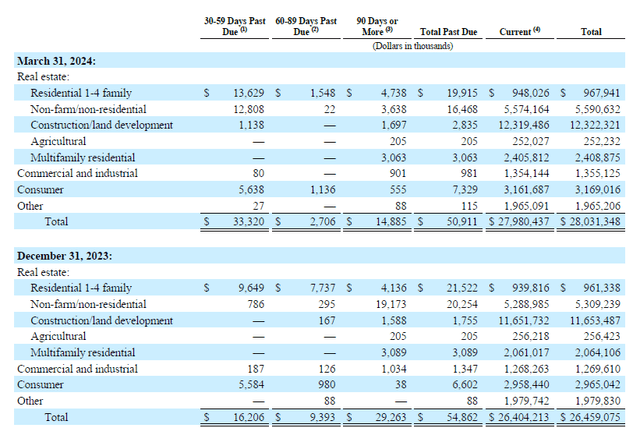

The relatively low LTV ratio also explains why the bank’s loan quality remains strong. In fact, in the first quarter of this year, the net amount of loans past due actually decreased on a QoQ basis. As you can see below, just under $51M of loans was classified as ‘past due’ on a total of in excess of $28B in loans.

Bank OZK Investor Relations

This means that despite seeing the size of the loan book increase by in excess of $1.5B, there was a decrease of $4M in the total amount of loans past due.

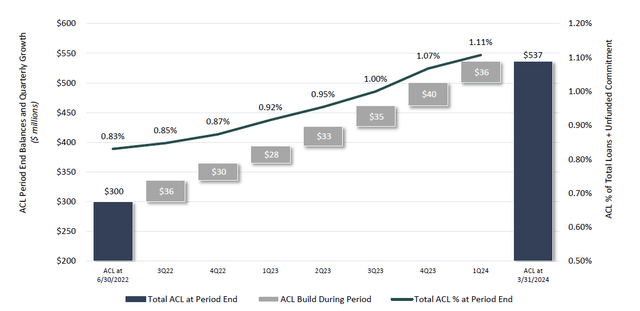

Meanwhile, the bank continues to add to its provisions, and in the past two years, it increased its total allowance for credit losses to $537M. This represents 1.11% of the total funded and unfunded loan commitments and represents about 10 times the total amount of loans that is currently past due.

Bank OZK Investor Relations

And of course, it’s not because a loan soured that Bank OZK will lose its entire investment. When an asset gets foreclosed and sold, the bank will always be able to recoup a substantial portion of its investment. And that’s why the RESG division was highlighted on the Q1 earnings call, as it ‘generates excellent returns with below-average risk’.

A closer look at the preferred shares again

As explained in a previous article, Bank OZK has one series of preferred shares outstanding, which is trading with (NASDAQ:OZKAP) as its ticker symbol. The preferred shares offer a 4.625% preferred dividend yield based on the $25 par value.

There are 14 million preferred shares outstanding, resulting in Bank OZK having to pay a preferred dividend of $16.2M per year, or $4.05M per quarter. As explained earlier in this article, the payout ratio is a low single digit percentage of the net income. The preferred shares can be called from November 2026 on.

Seeking Alpha

Last Friday, the preferred shares closed at $15.84, resulting in a yield of approximately 7.30% based on the current share price.

Investment thesis

Bank OZK is guiding for record earnings this year (this is backed by the consensus estimates calling for a $6+ EPS this year), increasing to in excess of $7 in 2026°, but the market is likely still a bit reluctant as the growth will mainly come from the Real Estate Specialties Group which means the total amount of commercial real estate on the balance sheet will likely increase. I’m fine with exposure to CRE, even if that exposure is a multiple of the total equity on a balance sheet, as the main thing that matters is how risky the loans are. As the RESG division has strict underwriting criteria and the LTV ratio is less than 50%, Bank OZK appears to be on top of things. Yes, CRE will be painful for some investors, but it will be the mezzanine and the equity tranches that will hurt the most. Banks with a 40-50% LTV ratio on projects should be able to deal with the fallout.

I have a long position in the preferred shares of Bank OZK, but I am also warming up to the common shares. The share price decreased in the recent past due to the Citibank downgrade, but the bank’s earnings profile remains robust, and the stock is now trading at less than 7 times earnings. I understand the market’s worries about the CRE portfolio, but as long as risk management is prioritized over growth, I think the risk/reward ratio is quite interesting at the current share price, which is just above the tangible book value of Bank OZK.